- November 21, 2023

- Posted by: Abishek Balakumar

- Category: Industries

Wealth and asset management firms are up against a tough trio of challenges: higher costs, slimmer profits, and customers who want more. So, how do they tackle this three-headed monster?

Well, there’s a new player in town – end-to-end third-party platforms. They’re like secret weapons that wealth and asset managers can use to tackle these challenges head-on.

These platforms bring some serious benefits to the table. They can help slash costs in the middle office and operations, open up exciting new business opportunities, and even create fresh revenue streams.

But here’s the kicker: picking the right platform isn’t child’s play. The top brass, including the CEO, must be in on it. It’s a two-step process. First, you’ve got to get a grip on your challenges, and second, take some savvy action to beat them.

Navigating Challenges in Wealth and Asset Management

Challenges abound! It’s a tricky trinity of rising costs, narrowing margins, and the ever-increasing demands of clients. Let’s break it down and see how these factors are reshaping the industry!

Note: Source information vetted from the BCG’s “Scalable Tech and Operations in Wealth and Asset Management.”

1. Escalating Costs in Technology and Operations

Major asset managers have seen their cost-to-income ratios (CIRs) gradually increase since 2018, reaching 74% in 2022. Smaller asset managers with less than $300 billion in Assets under Management (AuM) have experienced a more pronounced jump, reaching 78%. Meanwhile, in the wealth management sector, smaller players with AuM below $150 billion have encountered an even steeper rise, surpassing 82% in 2022. What’s fueling this surge in costs? It’s technology spending.

Notably, investments in application development and hosting have surged, reflecting the growing demand for new capabilities and the migration to the cloud. Moreover, the ever-evolving landscape of regulations adds another layer of complexity and cost.

2. Shrinking Margins and AuM

The industry faced an unprecedented event in 2022 when global Assets under Management declined by around 15%. This unfavorable outlook is exacerbated by the persistence of higher interest rates and sluggish GDP growth anticipated through 2025. Wealth and asset managers also find themselves caught in a web of relentless margin compression due to several market trends, including the growing presence of passive investments, digital competition, and the consolidation of industry giants. The result? A decline of 3% in return on assets (ROA) annually from 2018 to 2021.

Moreover, product fees have taken a substantial hit, with active funds experiencing an 11% decrease and passive funds witnessing a significant 35% drop since 2017. Model portfolio services have also seen a 12% margin reduction since 2017. Asset-servicing margins for typical wealth management mandates have plummeted to as low as 12 basis points. These challenges can be attributed to technology integration, scale advantages, and increased transparency.

3. Intensifying Client Demands

Client expectations are continuously on the rise, prompting wealth and asset managers to make significant investments. Notable areas of expenditure include hybrid advisory services, direct indexing, and managed portfolio solutions, all geared toward enhancing personalization. Clients increasingly seek complete transparency in their investments, particularly concerning sustainability and alignment with personal values. While fintech is a crucial enabler for wealth and asset managers to transform their business models, operational adjustments are equally critical for effectively adapting to the evolving landscape.

Given the formidable nature of these challenges, wealth and asset managers are exploring a viable solution – partnering with third-party service providers. As the industry transforms, outsourcing essential services becomes an attractive pathway to achieving operational efficiency and cost-effectiveness. This strategic shift allows wealth and asset managers to focus on their core competencies while efficiently addressing their multifaceted challenges.

Adapting Tech Solutions in Wealth and Asset Management

This surge directly responds to the escalating demand for streamlined digital experiences and automated operations. Notably, the share of third-party technology investment has soared by over 10% since 2018, impacting routine operations and strategic initiatives within wealth and asset management firms.

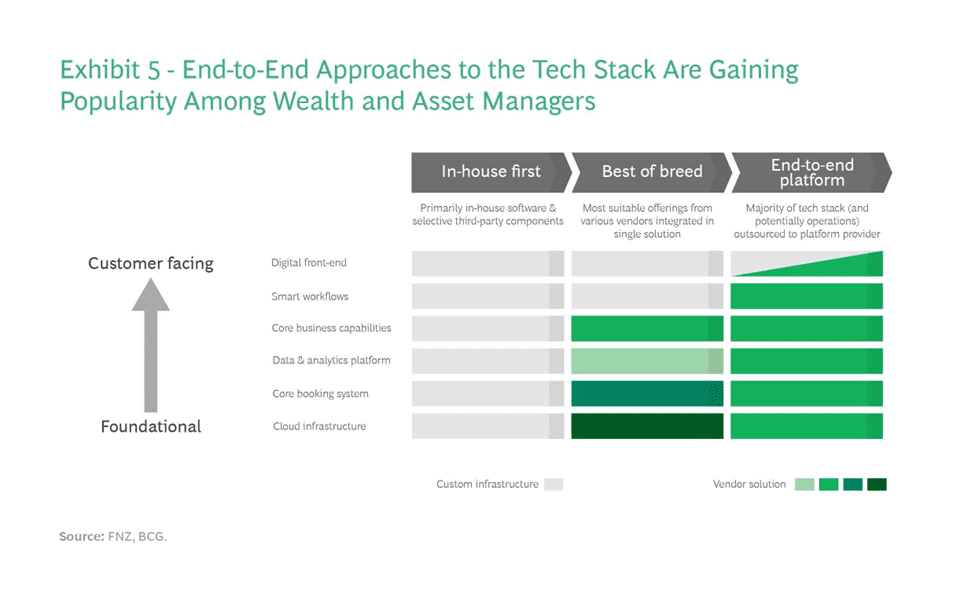

To comprehend these transitions, let’s deconstruct the conventional technology stack utilized by wealth and asset managers, identifying six key layers:

1. Digital Front End and Engagement: This layer is designed to provide multi-channel interfaces that manage customer and advisor interactions seamlessly.

2. Smart Workflows: These workflows structure, orchestrate, and automate processes, integrating them with various business solutions.

3. Core Business Capabilities: Offering product and service logic across the value chain, covering advisory, portfolio management, execution, and asset servicing.

4. Central Data and Analytics Platform: Acts as the hub for data ingestion, storage, and governance, enabling a unified client view and supporting AI and analytics-driven use cases.

5. Core Booking System: Functions as a central repository for customer and account data and transaction processing and facilitates reporting and third-party integrations.

6. Cloud Infrastructure: Essential for scalable computing and network resources, providing foundational services from developer tools to cybersecurity.

The most notable shift towards third-party solutions is observed in infrastructure and data layers, primarily driven by the migration of workloads to the cloud. A select few “hyperscalers” have seized the market by swiftly scaling computing resources and software architecture, a trend gaining traction due to cloud providers’ compliance with stringent data privacy and cybersecurity norms. Conversely, wealth and asset managers find opportunities for differentiation in the upper layers by focusing on well-designed customer journeys and seamless multi-channel experiences.

Embracing Novel Approaches to Technology and Operations

Traditionally, prominent players favored the in-house development of complex, stable operating models across major sections of their technology stacks. However, the evolving landscape of customer needs and the prevalence of software as a service (SaaS) solutions have led to an increasing adoption of a “best-of-breed” approach. This strategy involves integrating an expanded range of third-party solutions throughout the tech stack. While it expedites access to innovation, its successful implementation demands robust integration capabilities and rigorous architectural standards to manage the inherent complexity.

Moreover, as integration challenges persist, a growing trend is the deployment of end-to-end vendor platforms by financial institutions, covering non-differentiating activities. This approach significantly reduces the necessity for proprietary technology development and, in some instances, diminishes the reliance on in-house staff. Certain vendors offer outsourcing solutions for routine middle office and operations functions.

Although these vendor-based options were initially popular among smaller players or minor office locations of larger firms, they’ve recently gained traction among major incumbents. The pursuit of faster time-to-market strategies fuels this shift, the broader embrace of open finance and ecosystem use cases, and the scarcity of in-house tech expertise.

Of course, each approach has distinct benefits. The “in-house-first” and “best-of-breed” pathways afford control over technology specifications, customization, and differentiation while ensuring control over operational and security risks. Meanwhile, end-to-end platforms bring advantages like lower maintenance costs, automated upgrades, simplified integration, and greater flexibility for operational changes. For firms lacking the scale to independently develop and manage their solution stacks, an end-to-end platform emerges as a compelling option.

Taking the Bold Step

Wealth and asset management firms face significant challenges, prompting a need for digital and operational overhauls. Traditionally, in-house initiatives have encountered delays and budget issues, leading to a search for new solutions.

One emerging solution involves transferring certain tech aspects to end-to-end platforms. Vertically integrated providers offer services across the value chain, potentially leading to substantial cost savings. Alternatively, the “best-of-breed” approach allows institutions to pick solutions from various vendors but reintroduces some risks.

1. For leaders (CEOs, CTOs, and COOs), strategic decisions hinge on key considerations:

2. Flexibility: Does the new setup facilitate swift responses to market changes?

3. Coverage: Can it serve diverse markets and tap into new opportunities?

4. ROI: Is there a strong business case for savings or new revenue streams?

5. Vendor Reliability: Can the vendor be trusted for security, reliability, and innovation?

6. Alignment: Is the vendor relationship sustainable considering potential costs?

7. Migration: Can migration occur without compromising project benefits?

Ultimately, these new operating models provide opportunities for competitive advantages, driving innovation in an evolving industry landscape.